Illion Analytic Exercise

[Machine-Learning Python You have been given a file containing information on a number of loan applicants. Take the provided data set and attempt to identify what factors are useful in predicting loan performance. Report back on your findings, including any issues/concerns with the data.

Summary

Best machine learning model: Decision tree.

Model accuracy: 76.0%

Model precision: 98.5%

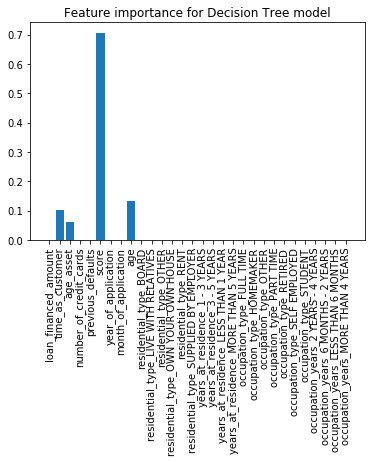

Feature importance (from high to low): Score, age, time as customer, and age asset.

Issues with the data:

- Imbalanced data. After cleaning, BAD loan records are only 4.25% (74/1740) of the whole data set.

- Many missing and inconsistent data entries.

- Some unreliable score values (negative values).

Data overview

The data has 3923 rows and 15 columns originally. A sample is as follow

date_of_application date_of_birth loan_financed_amount assessment_outcome \

0 22/12/2014 NaN 5349.0 Approved

1 11/12/2014 NaN 23350.0 Approved

2 9/01/2015 NaN 10497.0 Approved

3 5/12/2014 18-Jul-48 2920.0 NaN

4 9/12/2014 22-Jan-70 19466.0 Approved

5 5/12/2014 5-Jan-68 25350.0 NaN

6 5/12/2014 13-Dec-79 18850.0 NaN

7 15/12/2014 19-Aug-73 36240.0 Approved

8 7/12/2014 13-Nov-67 29240.0 NaN

9 8/12/2014 28-Aug-70 35750.0 NaN

time_as_customer age_asset residential_type years_at_residence \

0 130.0 New NaN NaN

1 28.0 New NaN NaN

2 27.0 New NaN NaN

3 NaN New RENT LESS THAN 1 YEAR

4 41.0 New NaN NaN

5 NaN 8+ OWN YOUR OWN HOME 1 - 3 YEARS

6 NaN New OWN YOUR OWN HOME 1 - 3 YEARS

7 28.0 New BOARD 1 - 3 YEARS

8 NaN New OWN YOUR OWN HOME MORE THAN 5 YEARS

9 NaN New RENT 1 - 3 YEARS

number_of_credit_cards occupation occupation_type \

0 0.0 NaN NaN

1 0.0 NaN NaN

2 0.0 NaN NaN

3 NaN RETIRED RETIRED

4 1.0 NaN NaN

5 NaN ADVISOR FULL TIME

6 NaN TECHNICIAN FULL TIME

7 0.0 CUSTOMER SERVICES FULL TIME

8 NaN TICKET INSPECTOR FULL TIME

9 NaN LABOURER FULL TIME

occupation_years previous_defaults score loan_performance

0 NaN 0 519 GOOD

1 NaN 0 650 GOOD

2 NaN 0 648 GOOD

3 MORE THAN 4 YEARS 0 715 NaN

4 NaN 0 717 GOOD

5 MORE THAN 4 YEARS 0 777 NaN

6 6 MONTHS - 2 YEARS 0 682 NaN

7 2 YEARS - 4 YEARS 0 561 BAD

8 MORE THAN 4 YEARS 1 523 NaN

9 2 YEARS - 4 YEARS 0 576 NaN

From the data, we would like to predict the loan performance to be either GOOD or BAD.

The Question

Maximize model precision.

From the data, the majority of loan performance is GOOD and there is only a very small portion of loan performance is actually BAD. Thus, correctly identifying the BAD loans is much more valuable than the GOOD loans. In practice, if a loan application is labeled as BAD, the application would not be proceeded, thus the lender would neither lose or gain money regardless on the prediction accuracy. However, if a loan application is predicted to be GOOD but turns out to be BAD, the lender would lose the lending money, so we want to eliminate this case. In other words, we want to maximize the probability that when a loan is predicted to be GOOD, its performance is actually GOOD. The technical term for this probability is precision. Hence, we will maximize the model precision in later analysis.

Data Preparation

Remove irrelevant columns

‘Occupation’ should not be a factor to determine loan performance. Other reason is that this column has too many non-numeric values so it is not useful for our model anyway.

‘Assessment outcome’ column has only 1 value ‘Approved’ or missing data. Thus, it will not provide any additional information to our model.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import collections

import sklearn

from sklearn.model_selection import train_test_split

from sklearn.tree import DecisionTreeClassifier

from sklearn.ensemble import RandomForestClassifier

from sklearn.linear_model import LogisticRegression

from sklearn.svm import SVC

from sklearn import neighbors

from sklearn.naive_bayes import GaussianNB

import pydotplus

# Set random seed

np.random.seed(1)

#Pandas options

pd.set_option('display.max_rows',200)

pd.set_option('display.max_columns',20)

pd.set_option('display.max_colwidth',20)

data_frame = pd.read_csv('TestData.csv')

#Drop irrelevant columns

data_frame=data_frame.drop(['assessment_outcome','occupation'],axis=1)

Drop missing data entry

#Drop missing data entry

data_frame.dropna(inplace=True)

Drop negative score

Negative scores may be legit and have some meanings. However, due to lack of explaination we do not include negative score in our analysis.

data_frame=data_frame[data_frame['score']>=0]

Convert time

Extract the following information as new columns: ‘age of applicant’, ‘year of application’, ‘month of application’.

#Convert date_of_application and date_of_birth into datetime

new_column=pd.to_datetime(data_frame['date_of_application'])

data_frame['date_of_application']=new_column

new_column=pd.to_datetime(data_frame['date_of_birth'])

data_frame['date_of_birth']=new_column

#Add year_of_application, month_of_application, and age into the data_frame

data_frame['year_of_application']=pd.DatetimeIndex(data_frame['date_of_application']).year

data_frame['month_of_application']=pd.DatetimeIndex(data_frame['date_of_application']).month

data_frame['year_of_birth']=pd.DatetimeIndex(data_frame['date_of_birth']).year

data_frame.loc[data_frame['year_of_birth']>2017,'year_of_birth']-=100

data_frame['age']=(2017 - data_frame['year_of_birth'])

#Drop redundance date_of_application, date_of_birth, year_of_birth

data_frame=data_frame.drop(['date_of_application', 'date_of_birth', 'year_of_birth'],axis=1)

Convert ‘age_asset’ to integer, remove the ‘+’ sign

#Convert age_asset to integer, remove the '+' sign

data_frame.loc[data_frame['age_asset']=='New','age_asset']='0'

data_frame['age_asset'].replace(regex=True,inplace=True,to_replace='\+',value='')

data_frame['age_asset']=pd.to_numeric(data_frame['age_asset'],errors='coerce')

Fix inconsistent data type

#Fix typo in data entry

#data_frame['residential_type'].unique()

#Out[173]:

#array(['BOARD', 'OWN YOUR OWN HOME', 'RENT', 'SUPPLIED BY EMPLOYER',

# 'LIVE WITH RELATIVES', 'OTHER', 'OWN', 'OWN YOUR OWN HOUSE'],

# dtype=object)

data_frame['residential_type'].replace(inplace=True,to_replace=['OWN','OWN YOUR OWN HOME'],value='OWN YOUR OWN HOUSE')

#data_frame['years_at_residence'].unique()

#Out[177]:

#array(['1 - 3 YEARS', 'MORE THAN 5 YEARS', 'LESS THAN 1 YEAR',

# '3 - 5 YEARS', '1', '4', '3 YEARS', '5 YEARS OR MORE',

# '1 - 2 YEARS', '1 YEAR', 'OVER 4 YEARS', 'OVER 1 YEAR',

# 'LESS THAN ONE YEAR', '1 YEAR OR MORE', '5 YEARS OR OVER',

# '1-3 YEARS', '3-5 YEARS', '3-5 YEARS'], dtype=object)

data_frame['years_at_residence'].replace(inplace=True,to_replace=['5 YEARS OR MORE','5 YEARS OR OVER'],value='MORE THAN 5 YEARS')

data_frame['years_at_residence'].replace(inplace=True,to_replace=['3 YEARS','OVER 4 YEARS','3-5 YEARS','3-5 YEARS','4'],value='3 - 5 YEARS')

data_frame['years_at_residence'].replace(inplace=True,to_replace=['1','1 - 2 YEARS','1 YEAR','OVER 1 YEAR','1 YEAR OR MORE','1-3 YEARS'],value='1 - 3 YEARS')

data_frame['years_at_residence'].replace(inplace=True,to_replace=['LESS THAN ONE YEAR'],value='LESS THAN 1 YEAR')

#data_frame['occupation_type'].unique()

#Out[180]:

#array(['FULL TIME', 'RETIRED', 'SELF EMPLOYED', 'PART TIME', 'OTHER',

# 'HOMEMAKER', 'STUDENT', 'FULLTIME', 'FULL'], dtype=object)

data_frame['occupation_type'].replace(inplace=True,to_replace=['FULLTIME','FULL'],value='FULL TIME')

#data_frame['occupation_years'].unique()

#Out[181]:

#array(['2 YEARS - 4 YEARS', 'MORE THAN 4 YEARS', 'LESS THAN 6 MONTHS',

# '6 MONTHS - 2 YEARS', '2 - 4 YEARS', '3 YEARS', '2 YEARS',

# '5 YEARS', '1 YEAR', 'OVER 4 YEARS', 'LESS THAN 1 YEAR',

# '1 YEAR OR OVER', '1 YEAR OR MORE', '5 YEARS OR MORE',

# '6 MOTHNS - 2 YEARS', 'LESS THEN 6 MONTHS'], dtype=object)

data_frame['occupation_years'].replace(inplace=True,to_replace=['5 YEARS','OVER 4 YEARS','5 YEARS OR MORE'],value='MORE THAN 4 YEARS')

data_frame['occupation_years'].replace(inplace=True,to_replace=['2 - 4 YEARS','3 YEARS','2 YEARS'],value='2 YEARS - 4 YEARS')

data_frame['occupation_years'].replace(inplace=True,to_replace=['1 YEAR','LESS THAN 1 YEAR','1 YEAR OR OVER','1 YEAR OR MORE','6 MOTHNS - 2 YEARS'],value='6 MONTHS - 2 YEARS')

data_frame['occupation_years'].replace(inplace=True,to_replace=['LESS THEN 6 MONTHS'],value='LESS THAN 6 MONTHS')

Convert non-numeric data into binary

#One-hot encode data

labels=data_frame['loan_performance']

data_frame=data_frame.drop('loan_performance',axis=1)

data_frame=pd.get_dummies(data_frame)

data_frame['loan_performance']=labels

Data Visualization

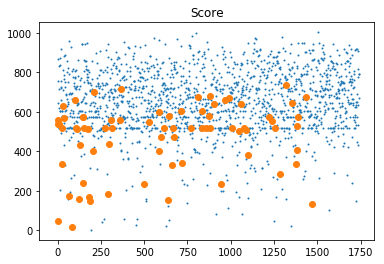

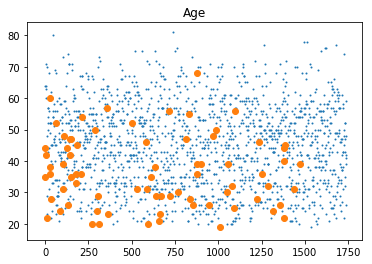

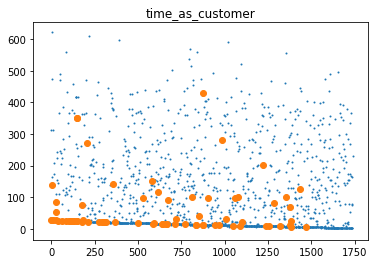

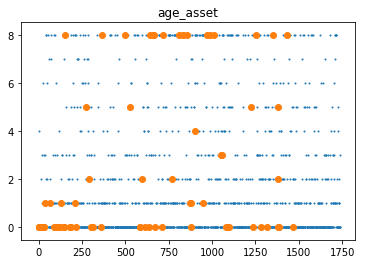

We scatterplot ‘score’, ‘age’, ‘time as customer’, ‘age asset’. The big dots are BAD loans and the small dots are GOOD loans.

# Visualize data

length=len(data_frame['score'])

mask=data_frame['loan_performance']=='GOOD'

good_index=[]

bad_index=[]

for i in range(len(mask)):

if mask.iloc[i]==True:

good_index.append(i)

else:

bad_index.append(i)

plt.scatter(good_index,data_frame['score'].loc[mask],s=1,label='GOOD')

plt.scatter(bad_index,data_frame['score'].loc[~mask],label='BAD')

plt.title('Score')

plt.show()

plt.scatter(good_index,data_frame['age'].loc[mask],s=1,label='GOOD')

plt.scatter(bad_index,data_frame['age'].loc[~mask],label='BAD')

plt.title('Age')

plt.show()

plt.scatter(good_index,data_frame['time_as_customer'].loc[mask],s=1,label='GOOD')

plt.scatter(bad_index,data_frame['time_as_customer'].loc[~mask],label='BAD')

plt.title('time_as_customer')

plt.show()

plt.scatter(good_index,data_frame['age_asset'].loc[mask],s=1,label='GOOD')

plt.scatter(bad_index,data_frame['age_asset'].loc[~mask],label='BAD')

plt.title('age_asset')

plt.show()

Dealing with Imbalanced Data - Up Sampling

Machine learning models need the number of data points in each class to be roughly in the same size in order to work properly. Otherwise, they will likely treat BAD loans as noise. One simple way to work around the problem is up sampling the minority data. It means replicating BAD loan data so that the number of BAD loan data is closely equal to the number of GOOD loan data.

First, we need to split the data into training set and testing set.

#Split the dataframe into train_frame and test_frame

mask=np.random.rand(len(data_frame))<0.75

train_frame=data_frame[mask]

test_frame=data_frame[~mask]

The training data will be up sampling to train our models. However the testing data will be kept intact and only be used for testing.

#Resampling bad loan data to balance the data classes between good and bad performance

bad_loan_data=train_frame[train_frame['loan_performance']=='BAD']

train_frame=train_frame.append([bad_loan_data]*10,ignore_index=True)

train_labels=train_frame['loan_performance']

train_features=train_frame.drop(['loan_performance'],axis=1)

test_labels=test_frame['loan_performance']

test_features=test_frame.drop(['loan_performance'],axis=1)

Now we are ready to train our models

Baseline Performance

Our baseline model assumes all application is GOOD. The folowing results are obtained with the baseline model for the data after cleaning:

Accuracy: 95.7% Precision: 95.7%

The main reason for this high performance is we only 74 records of BAD loans in the total of about 1700 records. Nevertheless, we are going to improve the precision number.

Model Training

We apply the training data set to a numbers of classification models including Naive Bays, K-nearest Neiboughs, Logistic Regression, Random Forest, Support Vector Machine, and Decision Tree.

###############################

NAIVE BAYES

Predicted BAD GOOD

Actual

BAD 9 8

GOOD 86 359

Model accuracy (probability of right prediction): 0.7965367965367965

Precision (Probability that a loan is actually GOOD after being predicted GOOD): 0.9782016348773842

###############################

K-NEAREST NEIGHBORS

Predicted BAD GOOD

Actual

BAD 2 15

GOOD 52 393

Model accuracy (probability of right prediction): 0.854978354978355

Precision (Probability that a loan is actually GOOD after being predicted GOOD): 0.9632352941176471

###############################

SUPPORT VECTOR MACHINE

Predicted BAD GOOD

Actual

BAD 5 12

GOOD 65 380

Model accuracy (probability of right prediction): 0.8333333333333334

Precision (Probability that a loan is actually GOOD after being predicted GOOD): 0.9693877551020408

###############################

LOGISTIC REGRESSION

Predicted BAD GOOD

Actual

BAD 5 12

GOOD 60 385

Model accuracy (probability of right prediction): 0.8441558441558441

Precision (Probability that a loan is actually GOOD after being predicted GOOD): 0.9697732997481109

###############################

RANDOM FOREST

Predicted BAD GOOD

Actual

BAD 1 16

GOOD 7 438

Model accuracy (probability of right prediction): 0.9502164502164502

Precision (Probability that a loan is actually GOOD after being predicted GOOD): 0.9647577092511013

###############################

DECISION TREE

Predicted BAD GOOD

Actual

BAD 12 5

GOOD 106 339

Model accuracy (probability of right prediction): 0.7597402597402597

Precision (Probability that a loan is actually GOOD after being predicted GOOD): 0.9854651162790697

##############################################

# NAIVE BAYES

clf = GaussianNB()

# Train the Classifier

clf.fit(train_features, train_labels)

# Use the forest's predict method on the test data

predictions = clf.predict(test_features)

# Print model accuracy and True Positive rate

print('###############################')

print('NAIVE BAYES')

Performance_Report(test_labels, predictions)

##############################################

# K-NEAREST NEIGHBORS

clf = neighbors.KNeighborsClassifier()

# Train the Classifier

clf.fit(train_features, train_labels)

# Use the forest's predict method on the test data

predictions = clf.predict(test_features)

# Print model accuracy and True Positive rate

print('###############################')

print('K-NEAREST NEIGHBORS')

Performance_Report(test_labels, predictions)

##############################################

#SUPPORT VECTOR MACHINE

clf = SVC(kernel='linear')

# Train the Classifier

clf.fit(train_features, train_labels)

# Use the forest's predict method on the test data

predictions = clf.predict(test_features)

# Print model accuracy and True Positive rate

print('###############################')

print('SUPPORT VECTOR MACHINE')

Performance_Report(test_labels, predictions)

##############################################

#LOGISTIC REGRESSION

clf = LogisticRegression(random_state=0)

# Train the Classifier

clf.fit(train_features, train_labels)

# Use the forest's predict method on the test data

predictions = clf.predict(test_features)

# Print model accuracy and True Positive rate

print('###############################')

print('LOGISTIC REGRESSION')

Performance_Report(test_labels, predictions)

##############################################

#RANDOM FOREST

clf = RandomForestClassifier(n_jobs=2, random_state=0)

# Train the Classifier

clf.fit(train_features, train_labels)

# Use the forest's predict method on the test data

predictions = clf.predict(test_features)

# Print model accuracy and True Positive rate

print('###############################')

print('RANDOM FOREST')

Performance_Report(test_labels, predictions)

##############################################

#DECISION TREE

clf = DecisionTreeClassifier(criterion = "entropy", random_state = 100,

max_depth=3, min_samples_leaf=5)

# Train the Classifier

clf.fit(train_features, train_labels)

# Use the forest's predict method on the test data

predictions = clf.predict(test_features)

# Print model accuracy and True Positive rate

print('###############################')

print('DECISION TREE')

Performance_Report(test_labels, predictions)

Factors that are useful to predict loan performance: score(71%), age(13%), time_as_customer(10%), and age_asset(6%).

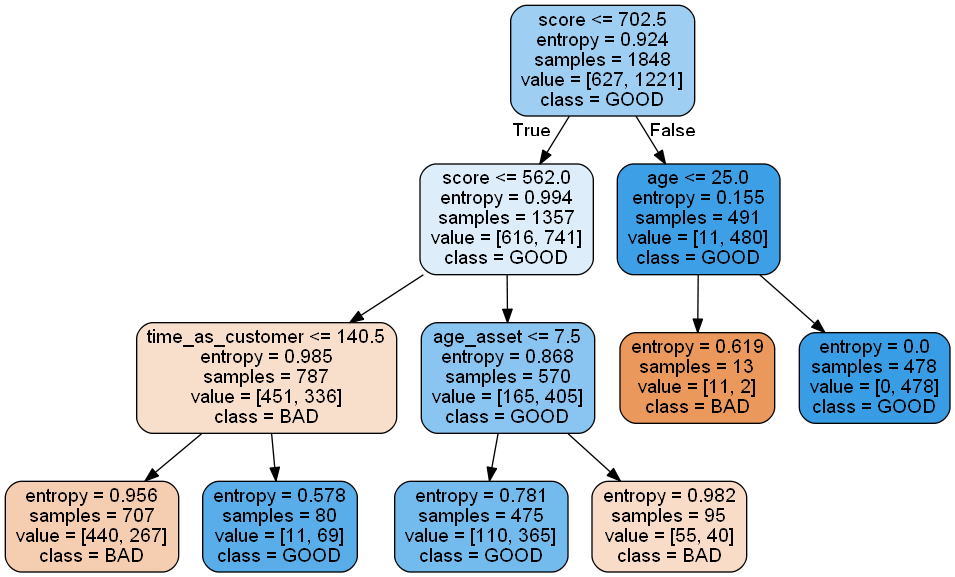

Tree Visualization

#visualization

data_feature_names = list(train_features)

data_class_names= list(train_labels)

# Visualize data

dot_data = sklearn.tree.export_graphviz(clf,

feature_names=data_feature_names,

class_names=data_class_names,

out_file=None,

filled=True,

rounded=True)

graph = pydotplus.graph_from_dot_data(dot_data)

graph.write_png('tree.png')

Archive

Machine-Learning Python Matlab Trading Strategy SQL R Algorithm